When Is Using Your 401(k) to Pay Off Debt a Good Idea?

Are you struggling to pay off debt? If so, consider using your 401(k) funds as an alternative repayment method. At the same time, this seems like a fast and easy way to chip away at large sums of money owed, but deciding if it's the right move for your overall financial situation can be tricky.

In this blog post, we'll explore when utilizing a 401(k) loan to pay down debt is an effective move – and discuss some potential pitfalls that come with withdrawing from retirement savings accounts early. If you're considering taking out a loan on your 401(k), make sure to weigh the pros and cons first before making any decisions.

The Rules on 401(k) Withdrawals

When it comes to utilizing your 401(k) funds to pay off debt, there are a few key rules you need to be aware of. First, most 401(k) plans will let you withdraw up to 50% of your vested balance for loan repayment.

When taking out a loan from a retirement plan, you'll also need to pay a fee and set up a repayment schedule with your plan administrator. When it comes time to repay the loan, you'll also have to pay income tax on any amount withdrawn.

Should You Use a 401(k) to Pay Off Debt?

Using a 401(k) to pay off debt can be an attractive option, especially for those with large amounts of debt that are overwhelming their monthly budget. There are pros and cons when considering whether or not this is the right move for your financial situation.

Withdrawals Before Age 59½

A loan is the most common way to use your 401(k) funds to pay off debt. When taking out a 401(k) loan, you can borrow up to 50% of the plan's balance or $50,000 – whichever is lower. However, there are some key things to be aware of when using this method.

When you take out a 401(k) loan, the funds must be repaid within five years, or you'll incur early-withdrawal penalties. If you cannot repay the loan within this time frame, it will be considered an early withdrawal and subject to taxes and a 10% penalty.

Another option is to withdraw early from your 401(k). When you do this, you can withdraw up to the amount of the debt you're trying to pay off. However, it's important to remember that any withdrawals before age 59½ are subject to taxes and a 10% penalty.

This means you'll need to be prepared to pay taxes on the amount withdrawn and should factor this into your decision. Additionally, it's important to note that any withdrawals before age 59½ can affect future contributions, as they may reduce the amount of money available for retirement.

Withdrawals After Age 59½

If you're over the age of 59½, then you may be able to withdraw funds from your 401(k) without incurring any early withdrawal penalties. When making withdrawals after reaching this age, you'll only be responsible for taxes on the amount withdrawn.

This means that if you have sufficient retirement savings, this could be a viable option for paying off debt without incurring the 10% penalty.

However, it's important to remember that any funds withdrawn after 59½ are not required to be repaid. This means that by withdrawing funds, you're reducing your retirement savings and could be jeopardizing your ability to meet your goals. When weighing your options, consider the long-term consequences of any withdrawals you make.

401(k) Loans to Pay Off Debt

If you're under 59½, taking out a loan on your 401(k) can be an effective way to pay off debt without incurring early withdrawal penalties. When taking out a 401(k) loan, you'll agree to repayment terms with your retirement plan provider and must make regular payments within the agreed-upon time frame.

Typically, these loans must be repaid within five years, and you'll need to make regular payments within this time frame to avoid any penalties. When taking out a 401(k) loan, remember that you're essentially borrowing from yourself and will be responsible for repaying the full amount with interest.

Additionally, suppose you leave your job or become disabled during the loan period. In that case, the remaining loan balance must be repaid by you within 60 days, or it will be considered an early withdrawal and subject to taxes and a 10% penalty.

401k loan to pay off debt calculator

When deciding whether or not to use your 401(k) funds to pay off debt, a 401(k) loan to pay off debt calculator can help. This tool allows you to input variables related to your current financial situation and potential repayment options.

For instance, you can assess the effects of paying down debt without tapping into retirement savings by entering all loan details, including interest rates, fees, and repayment schedules. You can also compare different scenarios to see which would be the most beneficial in terms of overall financial health.

By determining whether or not there are any tax benefits from using a 401(k) loan to pay off debt, you'll gain valuable insight into how this option might affect your bottom line. For example, when you repay the loan, it is usually treated as taxable income for that year.

However, if you're in a higher tax bracket when the loan is taken out versus what you'll be at when repayment begins, there may be some tax advantages to using a 401(k) loan to pay off debt.

It's important to remember that while utilizing a 401(k) loan can be a useful way to get rid of debt, and there are also some potential pitfalls. For example, if you change jobs or become unemployed during repayment, you may need help repaying the loan.

If you cannot repay the loan within the repayment term (usually five years), it becomes a taxable withdrawal and incurs an additional 10% penalty on top of the taxes due.

Whether or not using your retirement funds to pay off debt is smart depends on your financial situation. By consulting a 401(k) loan to pay off debt calculator and weighing the pros and cons, you can make an informed decision about whether or not this option is right for you. When done carefully, tapping into retirement savings can help you avoid financial hardship now – while still protecting your long-term financial security.

Benefits of Taking a 401(k) Loan to Pay Off Debt

Taking out a loan can greatly reduce high-interest debt if you're confident in making regular payments toward the 401(k) loan. You're borrowing from yourself when you take out a 401(k) loan.

You won't be subject to the same fees and penalties as other loan sources. Additionally, because of the tax-advantaged nature of 401(k) plans, you may save money on taxes by taking out a loan rather than withdrawing funds from the account.

Risks of Utilizing 401(k) Funds to Pay Off Debt

Although taking out a loan on your 401(k) can provide certain benefits, this strategy has potential risks. You risk your future by taking out a loan from your retirement account. If you default on the loan, you could owe taxes and penalties to the IRS.

Additionally, if you leave your employer for any reason before repaying the loan, you'll be required to pay back the original amount (plus interest) within a short period.

Check Your Eligibility

Before taking a loan out on your 401(k), double-check your eligibility. Most employers will allow you to borrow up to 50% of the assets in your account, but some have stricter rules – and some won't even permit it at all. Also, consider any fees or interest rates associated with a 401(k) loan.

Understand the Tax Implications

When you take a loan out on your 401(k), you are withdrawing money from a pre-tax retirement account, which can affect the taxes you owe. When taking out a loan, you must keep in mind that:

- When you repay the loan, your repayment is made with after-tax dollars.

- When it comes time to withdraw money from your 401(k) in retirement, you'll be taxed on the loan amount (if not already paid off).

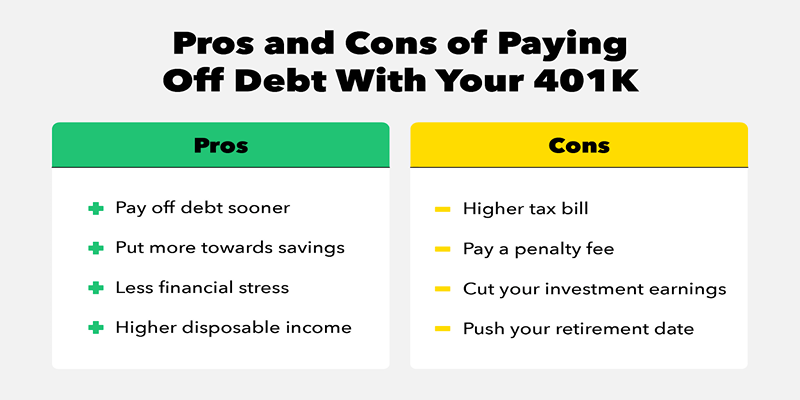

Pros and Cons

Pros

- A 401(k) loan can provide quick access to a large sum of money, making it an attractive option for those looking to pay off debt quickly.

- When you borrow from your retirement savings, there is no need to go through the process of applying for a loan or credit line with a bank or other lender.

- When you borrow from your 401(k), you are essentially using your own money and paying yourself interest, which can be a great way to save money in the long run.

Cons

- When you take out a 401(k) loan, your retirement savings are reduced, and so is their potential for growth over time.

- When you leave your employer, the loan must be paid back in full in a very short amount of time (usually within 60 days). If it is not repaid, the loan amount may be considered a taxable distribution and subject to income tax and an additional 10% penalty for early withdrawal.

- When taking out a 401(k) loan, you risk your retirement security, as the borrowed money will no longer earn compound interest.

FAQs

When Is Using Your 401(k) to Pay Off Debt a Good Idea?

Using your 401(k) to pay off debt can effectively manage large sums of money owed. When deciding if this is the right move for you, it's important to consider the potential consequences of withdrawing funds early and weigh the pros and cons.

Ultimately, taking out a loan or making an early withdrawal from your 401(k) should be a last resort. When considering any options, consult with a financial advisor and carefully evaluate the long-term consequences of your decisions.

Is the interest rate on my debt higher than what I would pay for a 401(k) loan?

If so, a loan on your 401(k) may make sense. When you borrow from your retirement account, the money is repaid with interest to yourself (since you own the account). The interest rates are usually lower than what most credit cards or other loans would offer.

Do I have an emergency fund?

One of the key considerations when taking out a 401(k) loan is the potential negative consequences if you cannot repay it. If your financial situation changes, having an emergency fund can help cover additional expenses and reduce the risk of defaulting on the loan.

Do I have other debt repayment options available?

It's important to consider other repayment strategies and how they compare to the 401(k) loan. If there are lower-interest debt consolidation options or even refinancing your home that could help you pay off the debt more quickly, these should be weighed against the pros and cons of taking out a 401(k) loan.

What type of repayment terms can I get for the loan?

Reviewing the repayment terms when taking out a 401(k) loan is important. Many plans allow you to repay the loan over five years, while some may have shorter or longer options available. It would help if you also looked into any early repayment penalties or other fees associated with the loan to ensure you make the best financial decision.

Conclusion

Taking out a loan on your 401(k) may be a good option for reducing high-interest debt if you weigh all of the pros and cons. When considering this strategy, it's important to ensure that you have an emergency fund to reduce the risk of defaulting on the loan. Additionally, you should compare other debt repayment options and what type of repayment terms you can get for the 401(k) loan. When utilized strategically, a 401(k) loan can be used to effectively reduce debt while still allowing you to save for retirement.

-When it comes to using your 401(k) as a debt repayment vehicle, there are a lot of things to consider. Before making any decisions, determine if this type of loan is the best move for your overall financial situation.